Thinking of Incorporating? You'll Need to Appoint a Registered Agent

What’s a registered agent? This is a commonly asked question of entrepreneurs who are new to the incorporation process. It is a statutory requirement that all entities appoint a registered agent, also known as resident agent or statutory agent, when incorporating. The registered agent can be an individual or business entity and must have a physical address in the state of incorporation. The primary responsibility of the registered agent is to receive legal correspondence on the entity’s behalf, in addition to, any official notices from the Secretary of State. Failure to maintain a registered office in the state of incorporation can cause the entity to fall out of good standing and even be declared Void if a new agent is not appointed.

Designation of the registered agent is typically made on the formation documents. There is often a misconception that the registered agent address is the same as the principal office address. This is not the case. The two are very different and serve different purposes. Most jurisdictions allow business  entities to maintain a principal place of business outside the state. If the business does not operate or maintain an address in the state of incorporation, a commercial registered agent can be appointed. If the business does operate or maintain an address in the state of incorporation, ie: director or officer, then either can be appointed as the registered agent of the entity.

entities to maintain a principal place of business outside the state. If the business does not operate or maintain an address in the state of incorporation, a commercial registered agent can be appointed. If the business does operate or maintain an address in the state of incorporation, ie: director or officer, then either can be appointed as the registered agent of the entity.

There are many benefits of appointing a commercial registered agent. The commercial registered agent maintains a physical address in the state and is staffed during normal business hours to accept all correspondence received on your company’s behalf. The registered agent’s address is kept on file with the Secretary of State and this information is stored as Public Record. Utilizing a commercial registered agent means that you need not worry about address changes or not receiving an important company document.

American Incorporators Ltd. provides this service nationwide & is ready to assist with all of your corporate needs. Contact us today!

Find the answers to all of your major incorporation questions in our new eBook

Topics:

Registered Agent,

forming a business,

registered agent Delaware,

create a corporation

Redesigned Website Provides Comprehensive Resources for  Companies Seeking to Incorporate

Companies Seeking to Incorporate

Wilmington, DE (PRWEB) March 17, 2015

American Incorporators Ltd., a firm that has been helping businesses form sustainable corporations and limited liability companies for over 35 years, announced the launch of a restructured and redesigned website at http://www.ailcorp.com with the goal of providing its current and prospective customers quick and easy access to critical resources and services.

“We pride ourselves on delivering a friendly and helpful experience for the businesses that come to us for formation and the many services we provide. We’re excited that the new American Incorporators website reflects that,” said Ann Chilton, Chief Executive Officer. “Our goal is to not only help businesses get up and running as credible corporations, but to work with them from inception and as they continue to grow and change over time.”

Visitors to the new site have access to valuable up-to-date information on starting and maintaining a business. The support services and pricing American Incorporators offers are described in detail on the updated site and available for purchase online. Additionally, the site prominently displays the many service options available to customers and new visitors, including live chat, robust FAQs and access to social media channels. Other key features include:...

To view the full press release click here

Topics:

LLC Creation,

Corporations,

incorporation process,

easy incorporation,

starting a business,

C Corporation

Annual tax payments for Delaware Corporations are due this Sunday March 1. The deadline is NOT extended because it falls on Sundaym if payment is not received by Sunday the state will add a non-negotiable late fee.

Due to the fact that the deadline falls on a weekend American Incorporators' office will be open 8am-6pm through Friday this week to assist in your annual payments. Please call 800.421.2661 to speak with a specialist or visit http://bit.ly/1Ft6cn0 to pay online.

Topics:

Reminders

American Incorporators loves to provide small business tips to small business owners

and entrepreneurs. We have searched to create a list of the best apps for small business owners.

Expensify: Expensify is available for iOS and Android devices. This app makes keeping track of business expenses while on a business trip a breeze. The app also allows users to link up a credit or debit card, when expenses

Trello: Trello is an application and also accessible through trello.com that allows teams to collaborate on projects without clogging up email. Trello uses a systems of boards where teams can tag others, comment, and move cards to show completed, to-do, or need to complete projects,

Evernote: Evernote is a cloud-based app that syncs documents through all of your devices. This allows you to view edit and share documents as needed on all devices. Evernote is available for Android, iOS and evernote.com.

Pocket Analytics: This app allows you to visualize your analytics between multiple sources. Pocket Analytics syncs with Google Analytics, Flurry, Piwik, Facebook, Pingdom, and more. Unfortunately, Pocket analytics is only available for iOS.

Google Hangouts: Google Hangouts is a free messaging app that provides free video call for up to 10 people and free group chats for up to 100 people. Google Hangouts also allow you to make phone calls, and calls to other Google Hangouts users for free. Google Hangouts is available on Android, and iOS devices as well as web.

For More resources visit Our Small Business Resource Center.

Find the answers to all of your major incorporation questions in our new eBook

Topics:

Tips & Tricks

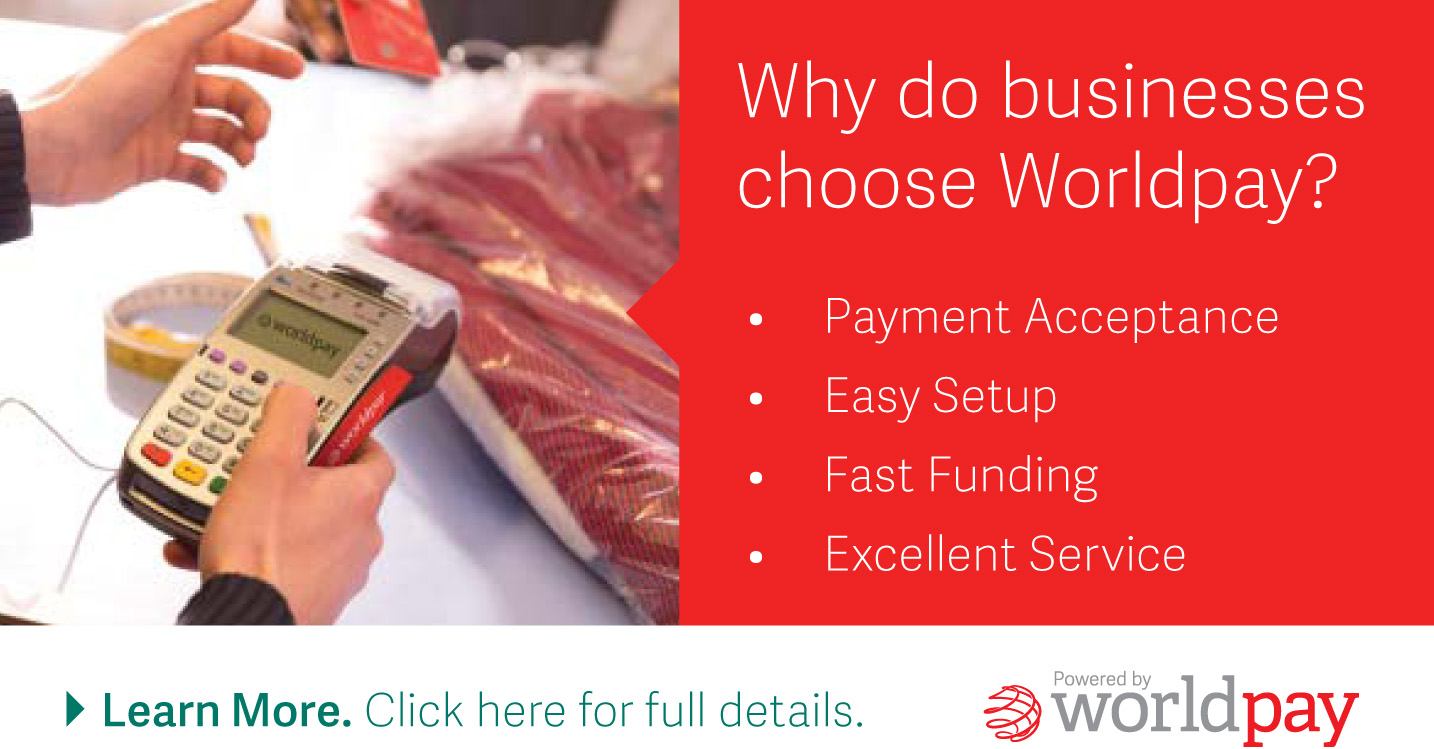

American Incorporators Ltd.is excited to announce that Worldpay is our newest preferred payment processing provider.

Worldpay is a leading global payment processor that allows businesses just like yours to accept all payment types including in-person, at the point-of sale, online and on-the-go via mobile devices.

Worldpay offers its clients:

- Mobile from Worldpay turns your mobile device into a hand-held terminal that accepts all major credit or debit cards.

- Virtual terminal allows you to take payments in person or over the phone using your existing computer or tablet. It requires no technical setup and provides real-time reporting to keep track of payments.

- An integrated cash register system accepts all major payment types and provides 24/7 access to real-time transaction reporting.

Worldpay can also help you navigate the compliance requirements related to Payment Card Industry Data Security Standard (PCI DSS) guidelines and the upcoming EMV (smart card) requirements. By October 1, 2015 all merchants must have EMV terminals in order to avoid penalty. The cost of noncompliance can be steep, including damage to your brand, costly fines, and loss of credit card processing privileges. For extra protection against data breaches, Worldpay also offers end-to-end encryption services.

For a limited time Worldpay is offering merchants a cash-back incentive of up to $750 per location. To access this deal fill out this short web form found here and Worldpay will contact you to get started

-1.jpg?width=415&height=216&name=web_banner_(344x190)-1.jpg) .

.

Topics:

credit card,

payment processing,

small business,

small business tips

What is an LLC?

The Limited Liability Company is a relatively new entity type that was developed towards the end of the 20th century as an alternative to a corporation. Modeled after a German entity type (GmBH), the US LLC originated in Wyoming in the late 1970s, emerged in Florida a decade later and by the early 1990s existed in all US jurisdictions. Since that time limited liability companies have steadily gained in popularity largely because they combine liability protection previously reserved for corporations with single taxation of partnerships. LLCs also have fewer requirements than corporations making them easier to maintain. LLC's are separate and distinct from its owners who are called "members." LLC's do not issue shares of stock like C Corporations and S Corporations. If you would like to read about S Corps and C Corps check out our blog here.

Ownership/ Member details about LLC's

There are 2 ways to reflect ownership of an LLC. It can be reflected as a percentage or by membership units which are similar to shares of stock in a corporation. The number of members of an LLC is unlimited and members can be individuals, partnerships, corporations, trust, nonresident aliens, etc.

Things to know about LLC's

- Limited Liability- Absent any specific personal guarantees, the amount at risk for members is limited to their investment in the LLC. The personal assets of the members are generally beyond the reach of creditors. This protection is for all members of the LLC unlike an LLP where one general partner must remain liable for partnership debts.

- Tax Benefits- LLC members may also enjoy the same flow-through tax benefits which are applicable to partners of a partnership.

- Easier to maintain- LLC's are not required to hold annual meeting and to record meeting minutes. LLC's are known for their operational ease.

- Heightened Credibility- Forming your company into an LLC can increase the credibility associated with your business.

Topics:

LLC Creation,

Limited Liability Companies,

incorporate now,

incorporate today,

Asset Protection,

s corp,

fast incorporation,

c corp

What is a C Corporation?

A C Corp is legal structure that businesses establish that is a separate entity from the owners and the people that manage it. Corporations are owned by their shareholders, and provide owners limited liability. C Corporations are the most widely type of entity for businesses large and small that have shareholders.

What's the difference between a C Corp and an S Corp?

All corporations both S and C are started as a C Corp. Once the C corp is formed the business has 75 days to to elect to become an S Corporation. This election is done with the IRS. More information abour S Corporations can be found Here.

Some things to know if you're thinking about starting a C Corporation

- C Corporations may have an unlimited amount of shareholders

- Owners do not need to be citizens or residents of the United States

- C Corporations shares may be owned by another business

- C Corporations are required to have bylaws, hold annual meetings and keep accurate record of the meeting minutes.

- Corporations can raise capital by through the sale of their stock.

If you want to incorporate your company don't worry, American Incorporators Ltd. provides fast and easy incorporation services for you so just give us a call at 800.421.2661 or Click Here for more details.

Topics:

Corporation Creation,

Corporations,

incorporation,

easy incorporation,

s corp,

s corporation,

starting a business,

c corp,

create a corporation,

what is a c corporation,

C Corporation

.jpg?width=240&height=180&name=0002-growth-graph_(1).jpg)

What is an S Corporation?

An S Corporation also know as S Corp is a legal entity described by IRS.gov as "a corporation that decides to pass income, loss, deductions, and credits to their shareholders." S corporations avoid the double taxation inherent to general business corporations, in which profits and dividends are both taxed.

How do I turn my business into an S Corp?

All corporations are started first as C Corporations. After your C Corporation is started your company must elect to become an S Corporation with the IRS by signing IRS form 2553.

Some things you need to know if you're starting an S Corp are

- Limit of Shareholders- S Corporations are limited to 100 shareholders

- Shareholder Definitions- A new law allows "members of a family" to qualify as one, and defines "members of a family" as the common ancestor, the lineal descendants of the common ancestor, and the spouses or former spouses of the lineal descendants or common ancestor

- Stock Restrictions- S Corporations only have one class of stock

- IRS filing- To obtain S Corporation status, all shareholders must sign IRS form 2553 which must be filed within 75 days of starting business.

If you want to incorporate your company don't worry, American Incorporators Ltd. provides fast and easy incorporation for you so just give us a call at 800.421.2661 or check our our website for more details.

Topics:

Corporations,

incorporate now,

incorporate today,

incorporation,

easy incorporation,

s corp,

s corporation,

what is an s corporation,

fast incorporation,

create a corporation,

starting an S corp,

incorporate your company

Incorporating your business can give you and the other owners of your business a number of benefits. For the benefits of incorporating you can look HERE. Incorporating your business can be an easy task with your friends at American Incorporators Ltd. to help you. It takes completing these simple tasks and we’ll be there to help you along the way

Incorporating your business can give you and the other owners of your business a number of benefits. For the benefits of incorporating you can look HERE. Incorporating your business can be an easy task with your friends at American Incorporators Ltd. to help you. It takes completing these simple tasks and we’ll be there to help you along the way

1) To be a legal entity you must register your business name with the Secretary of State. If you have already thought of your name check it HERE to make sure it is available in your state. If you do not already have a name, that’s okay think of a creative name for your business that will be attractive for customers.

2) Decide what kind of entity you would like to incorporate. LLC, S Corp, C Corp and what state you would like to incorporate in.

3) Call Us- 800-421-2661

4) Depending on your states regulations we could get your documentation and your business up and running in just a few days.

If you want to download our "How To Incorporate a Business With American Incorporators Ltd" Guide click HERE

Topics:

LLC Creation,

Tips & Tricks,

Start a Business From Home,

Limited Liability Companies,

incorporation process,

incorporate now,

incorporate today,

how to start a business,

incorporation,

forming a business,

easy incorporation

From July 15, 2014 until July 25, 2014 for every Facebook Post you share to your friends or every Tweet you retweet to your followers you'll be entered in our contest to win one Free, yes one FREE year of registered agent service in the state of your choice up to $149. Make sure to follow @AmericanIncLTD on twitter and like American Incorporators Ltd on Facebook to stay up do date with us.

From July 15, 2014 until July 25, 2014 for every Facebook Post you share to your friends or every Tweet you retweet to your followers you'll be entered in our contest to win one Free, yes one FREE year of registered agent service in the state of your choice up to $149. Make sure to follow @AmericanIncLTD on twitter and like American Incorporators Ltd on Facebook to stay up do date with us.

For more details about the contest click the link here: http://hub.am/1rqRPK4

Topics:

Tips & Tricks,

Registered Agent,

how to start a business,

registered agents,

starting a business,

registered agent USA,

registered agent Delaware

Call:

Call:  Live Chat

Live Chat